The United States has imposed has created banking regulations to prevent unnecessary damage to confidence and liquidity in the financial system. The regulations are meant to prevent things like bank runs, credit crunches, and financial crises.

Reasons for Banking Regulations in the U.S.

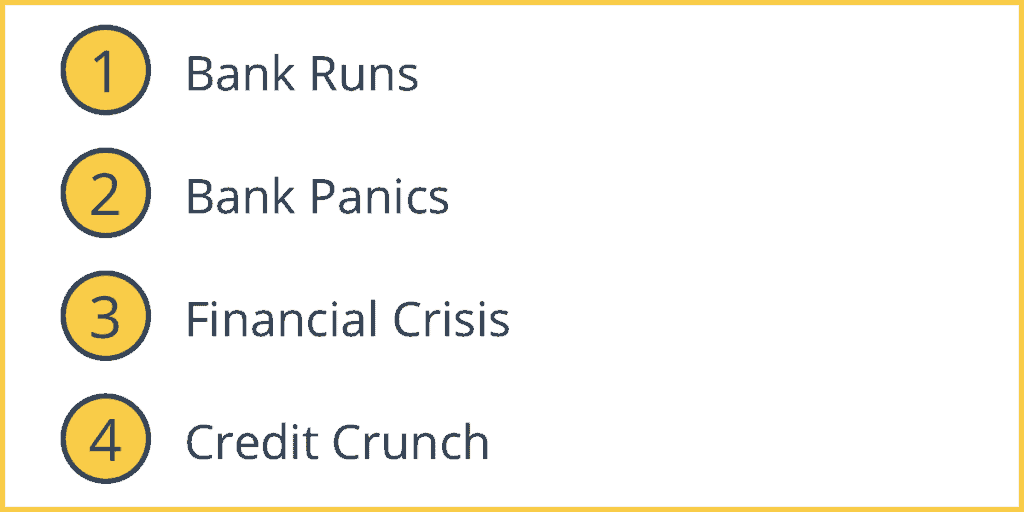

1. Bank Runs

Bank runs occur due to fears of insolvency. For this reason, the Federal Deposit Insurance Commission (FDIC) guarantees all bank deposit accounts up to $250,000.

2. Bank Panics

Bank panics is the plural of bank runs (because there is a fear of contagion across the banking system). This leads to systematic risk.

3. Financial Crisis

A financial crisis is a general breakdown of the financial system.

4. Credit Crunch

A credit crunch occurs when it is difficult to get credit.

Government Safety Nets

- To protect depositors and investors.

- To protect bank customers from monopoly exploitation.

- The safety nets keep the financial system stable.

- To play the role of lender of last resort – the Federal Reserve lends to banks when banks are short of funds and cannot borrow from other sources. The Fed lends until insolvent banks are healthy again. However, there is a moral hazard that makes banks take risks in which if they succeed they make a lot of money, but if they fail they get bailed out. This is a “too big to fail policy”.

Regulating Bodies

1. For Commercial banks

The FDIC, The Federal Reserve, state authorities and The Office of Comptroller of Currency.

2. For Saving banks

The Office of Thrift Supervision, FDIC and state authorities

4. For Credit Unions

National Credit Union and State authorities