The Efficient Market Hypothesis (EMH) is an application of ‘Rational Expectations Theory’ where people who enter the market, use all available & relevant information to make decisions. The only caveat is that information is costly and difficult to get.

This Efficient Market Hypothesis implies that stock prices reflect all available and relevant information, so you can’t outguess the market or systemically beat the market. This means it impossible for investors to either purchase undervalued stocks or sell stocks for inflated prices. There are three forms of market efficiency.

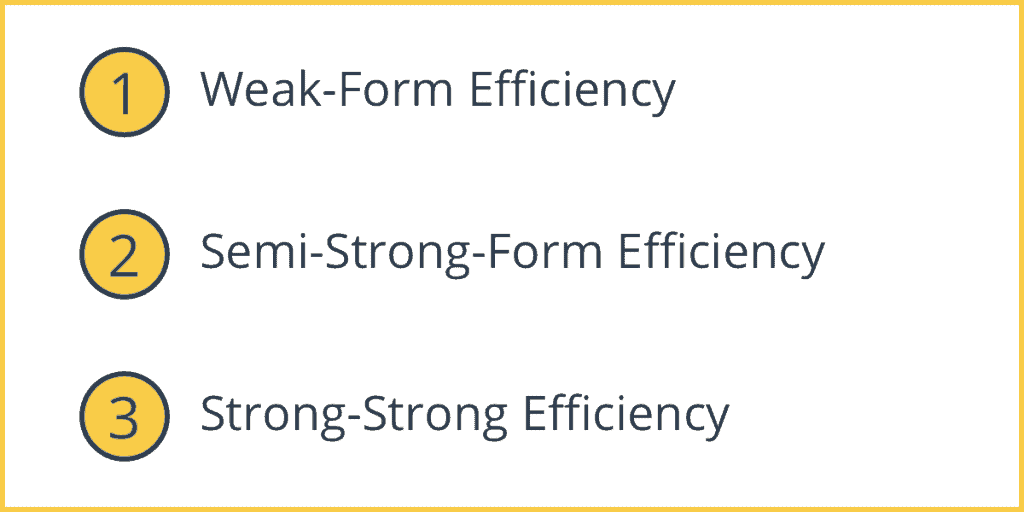

Forms of The Efficient Market Hypothesis

1. Weak-Form Efficiency

Future prices cannot be predicted by analyzing prices from the past meaning there are not meaningful patterns to gain from past performance. Future price movements are determined entirely by information not contained in the price series.

2. Semi-Strong-Form Efficiency

In a semi-strong-form efficiency, share prices adjust to publicly available new information very rapidly and in an unbiased fashion, such that no excess returns can be earned by trading on that information.

3. Strong-Strong Efficiency

In the strong-form market efficiency, the share prices reflect all information, public and private, and no one can earn excess returns.

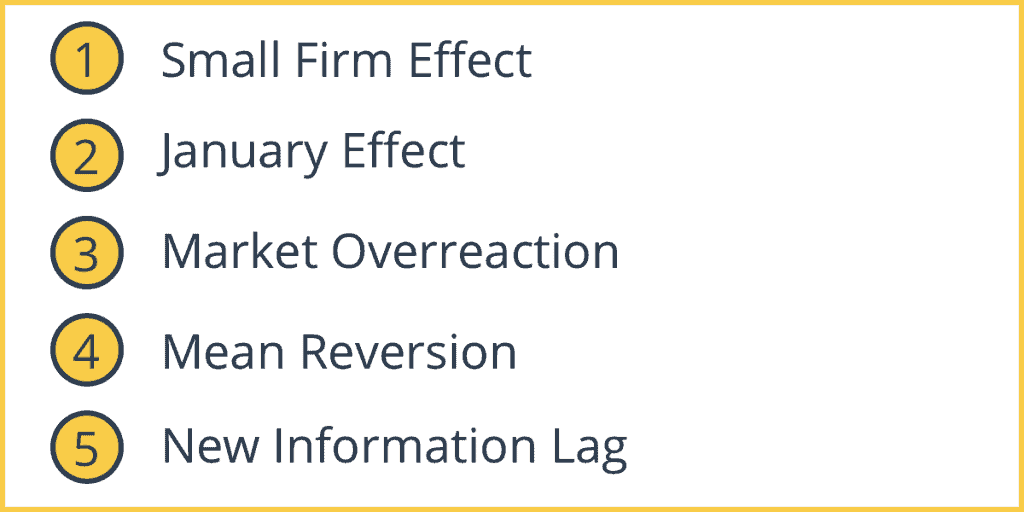

Evidence against the Efficient Market Hypothesis (EMH)

1. Small Firm Effect

Smaller firms tend to pay a higher risk-adjusted return than they should be paying.

2. January Effect

Stocks rally in January, from December going into January. There is no change in investor behavior.

3. Market Overreaction (Excessive Volatility)

The market tends to react to good/bad news more severely than they should.

4. Mean Reversion

If you look at stocks over a long period, a stock that was doing badly for that period of time will eventually do better for that same period of time.

5. The Incorporation of New Information is Slow

New information may not be represented adequately or may take time.