In monopolistic competition, there are many small firms who all have minimal shares of the market. Firms have many competitors, but each one sells a slightly different product. Firms are neither price takers (perfect competition) nor price makers (monopolies).

What is Monopolistic Competition?

An industry with many firms offering goods and services that are quite similar, but not identical, exists in a market structure of monopolistic competition. A monopolistic competitive industry has low barriers to both entry and exit. Monopolistic competition is effectively a state existing between perfect competition (which is itself theoretical) and monopoly, so it involves features of each market structure. Monopolistic competition can be considered to be a type of imperfect competition.

This is different than a monopoly because firms in a monopolistic competitive industry do not have the power to raise prices or set curtail supply so as to increase profits. Firms will typically respond to this kind of competitive situation by attempting to clearly define the differences between their goods/services and those of their competitors. They use a great deal of intensive marketing and advertising. In this way, these firms can gain above-market returns.

The market structure of monopolistic competition was first labeled in the 1930s, by two economists: the American economist Edward Chamberlin, and the English economist Joan Robinson.

Monopolistic Competition and Decision-Making

Choices made by one firm do not have an effect on the choices of the other firms in that industry that are competing with it. This is because there are many firms in the industry; one firm making a decision does not trigger a significant chain reaction. In an oligopoly, price wars can be triggered by one firm choosing to make a price cut; for monopolistic competition, this kind of cause-and-effect does not occur.

Monopolistic Competition and Advertising: Wasteful or Beneficial?

The high quantity of advertising that takes place in cases of monopolistic competition is sometimes critiqued by economists as uneconomical and inefficient. Some economists consider this to be a significant social cost. Companies managing situations of monopolistic competition tend to spend enormous amounts of their resources on advertising and marketing.

Only when the competing products have genuine differences is such advertising useful, as it provides more information to consumers so that they are better educated about consumption choices. But when the products are really devoid of any significant differences (which is common in monopolistic competition), this advertising falls under the umbrella of high-waste rent-seeking behavior. This leads to a deadweight loss for society as a whole.

Monopolistic Competition Means Small Firms Survive

Small businesses survive primarily in monopolistically competitive markets. In modern economies, monopolistic competition does promote the survival of smaller firms.

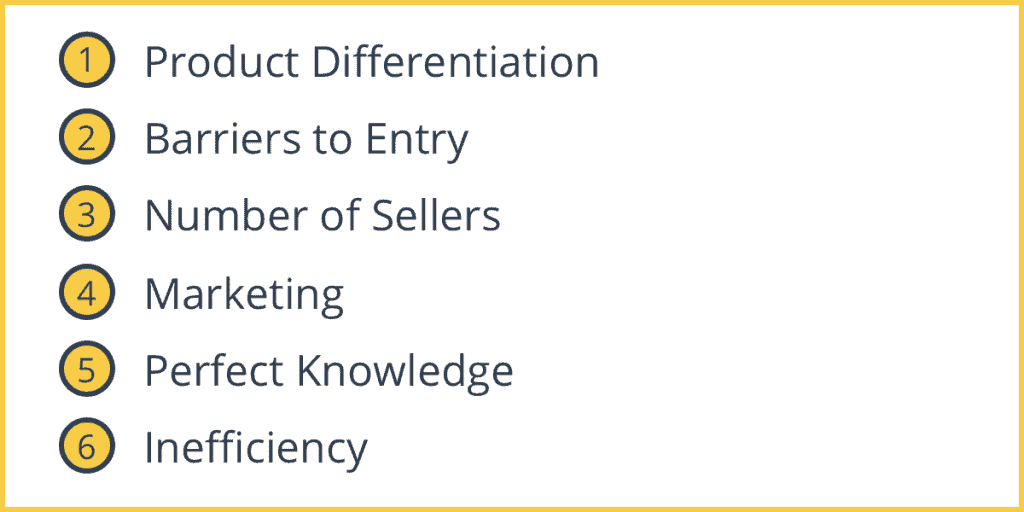

Characteristics of Monopolistic Competition

1. Product Differentiation

Products are differentiated (based on things like service, quality, or design). The product of a firm is close, but not a perfect substitute for another firm. This differentiation gives some monopoly power to an individual firm to influence the market price of its product.

This differentiation can be categorized into four different groups:

- Physical product differentiation: The way a product looks, including its color, size, shape, and so forth.

- Marketing differentiation: Firms use unique, eye-catching packaging that differs from that of other brands. Consumers remember this packaging and are ideally drawn to those products again.

- Human capital differentiation: This involves defining the unique value of a brand based on the employees’ skills, their degree of training, and even the look of their uniforms.

- Distribution-based differentiation: Using a different kind of distribution method, such as selling products online, can draw in new customers and increase profits.

2. Barriers to Entry

There are low barriers to entry. It ensures that there are neither supernormal profits nor any supernormal losses to a firm in the long run.

3. Number of Sellers

There are large numbers of firms selling closely related, but not homogeneous products. Each firm acts independently and has a limited share of the market. So, an individual firm has limited control over the market price.

4. Marketing

Products are differentiated, and these differences are made known to the buyers through advertisement and promotion. These costs constitute a substantial part of the total cost under monopolistic competition.

5. Perfect Knowledge

There is imperfect knowledge in the market. People don’t know who is selling the good the cheapest or who has the best quality. Sometimes a higher-priced product is preferred even though it is of inferior quality.

6. Inefficiency

Firms experience inefficiency in both the allocative and the productive senses.

Monopolistic Competition Examples

There are examples of monopolistic competition to be found throughout the economy. One well-known example is that of the athletic shoe market. When you walk into a sports store to buy running shoes, you will find a huge number of brands, like Nike, Adidas, New Balance, ASICS, etc.

So what does that look like? Let’s break that down:

- On the one hand, the market for running shoes seems to be full of competition, with thousands of competing brands and low barriers to entry.

- However, on the other hand, the market seems to be monopolistic, due to the uniqueness of each shoe brand and their power to charge a different price.

Other examples include:

- Competing coffee shops on one block in a city: Coffee shops are not just competing to show that their cups of coffee are the cheapest. They often emphasize the high quality of their coffee as well.

- TV shows: There are an enormous number of TV shows in the United States and internationally, many appealing to various niche audiences. This is a perfect example of one of the benefits of monopolistic competition: a huge amount of consumer choice.

- Consumer services (e.g. hairstyling): Different hair stylists will attempt to distinguish themselves and develop a good reputation based on how good their results are.

- Clothing: Virtually identical T-shirts will have vastly different value depending on the brand with which they are associated. A designer label can increase the price by ten times or more.

As these examples demonstrate, differentiation is a key element of monopolistic competition, so monopolistic competition tends to arise when differentiation is a viable option.

Monopolistic Competition versus Related Concepts

Perfect Competition versus Monopolistic Competition

In the case of monopolistic competition, businesses have differentiated products and are not price takers. These businesses have inelastic demand.

To sum up the differences and similarities:

- Nature of entry barriers: Monopolistic competition has low barriers to competition; perfect competition has no barriers to competition.

- Number of competing sellers in the industry: There are numerous producers in the market for both forms of competition.

- Businesses’ control over prices: Businesses do have some degree of control over their own prices in monopolistic competition, and no control over their own prices in perfect competition.

- Need for marketing: Branding and marketing are crucial for monopolistic competition because they are the central form of competition aside from pricing in this structure. Marketing does not matter in perfect competition.

- Resultant long-run allocative efficiency: With monopolistic competition, allocative efficiency does not result (P > MC). With perfect competition, there will be allocative efficiency in the long run (Price = MC).

- Resultant long-run productive efficiency: As with allocative efficiency, productive efficiency does not result from monopolistic competition in the long run, while it does result from perfect competition over a longer time span.

Monopoly versus Monopolistic Competition

Unlike in the case of a monopoly, where there is monopolistic competition, there should not be barriers to entry for an industry. This means that the market is competitive in the long run; firms amass normal profit.

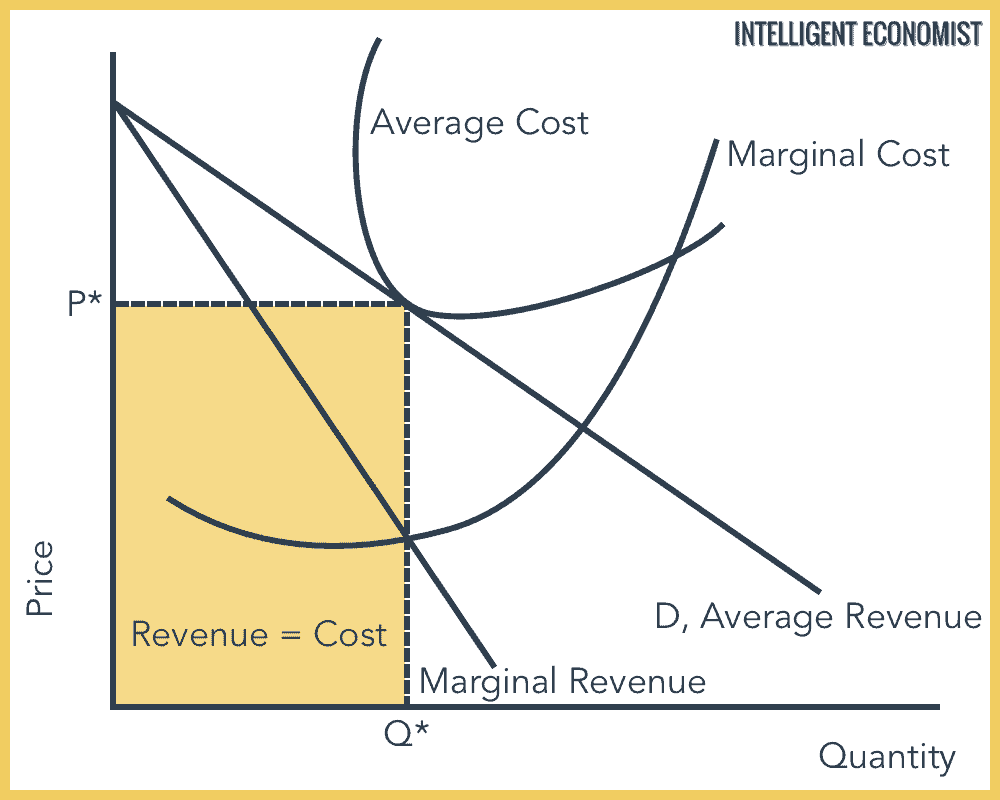

Monopolistic Competition: Short & Long-Run Equilibrium

The Monopolistic Competition graph is the same as the monopolies graph. The firm has the same short and long equilibrium and makes zero economic profits. Using the Profit Maximization Rule, MC = MR, we can find the quantity and draw a vertical line to the Demand curve, and thus find the corresponding price. The cost is found by drawing a vertical line from where Quantity meets the Average Cost curve to the price line.

Any signs of supernormal profits would create an incentive for more firms to enter the market, and since there are low barriers to entry, companies will join to make supernormal profits. This process will continue until everyone makes normal or zero economic profits in the long run. Even though normal profits are break-even, it includes profits for the entrepreneur for taking on risk.

Even though there is allocative inefficiency (where Price exceeds Marginal Cost) in monopolistic competition, there is a greater variety of products for the customer to select. However, costs rise because firms are forced to spend money on advertising.

Economic Profits and Monopolistic Competition

Firms can gain very high profits in the short run, but this does not typically last. Since there are low barriers to entry, other businesses will begin to pop up and try to gain a share of these profits themselves. This means higher and higher competition, which eventually results in a complete lack of any economic profits.

Note that economic profits are to be distinguished from accounting profits—for example, businesses can have no economic profit whatsoever and still have a positive net income, because net income accounts for opportunity cost as well.

Benefits and Drawbacks of Monopolistic Competition

Benefits:

- Because there are relatively few barriers to entry, and those that exist are not severe, markets are fairly contestable.

- The broad differentiation involved in monopolistic competition means there is a great deal of utility, diversity, and choice.

- Markets are more efficient than in true monopolies, although less allocatively or productively so than in perfect competition.

Drawbacks:

- Differentiation does not always lead to utility; it can also lead to pointless waste. Also typically wasteful is the high level of advertising associated with monopolistic competition, as various competing firms attempt to make clear to consumers the unique benefits of their goods and services.

- In a situation of profit maximization, allocative inefficiency arises in the short- and long-run. This takes place because the price goes above marginal cost in both the short- and long-run. Firms are less allocatively inefficient in the long run but are still so. The graph below demonstrates this issue.

Monopolistic Competition Graph

When supernormal profits occur in an industry, new businesses choose to enter the market in order to gain a share of these profits. The result is that the demand curve for existing firms is moved toward the left. Over time, new businesses will keep entering the market, with the eventual result that there are only normal profits left to be made. When this happens, businesses can be considered to have achieved long-run equilibrium.

This pattern explains why businesses benefit most from monopolistic competition in the short-run; in order to delay the arrival of that long-run equilibrium, firms will persist in creating new goods and services while attempting to differentiate their products even more.

How is the Monopolistic Competition Model Limited?

Models help us to understand real-world phenomena, but they can hardly be expected to be absolutely perfect or to describe every aspect of complex economic situations. The model of monopolistic competition can overlook the followings:

- Assuming normal profits is not always accurate. In the real world, many industries with monopolistic competition have extremely high profits.

- There can in fact be significant barriers to entry in the form of existing businesses’ very distinct differentiation and establishing customer loyalty. This makes it harder for new businesses to enter the industry.

- Because some businesses do have better differentiation for their brand, they can accrue supernormal profits.